(& DETAILS REGARDING ITS UNIT OF ACCOUNT)

A unit-of-account in financial accounting refers to the words that are used to describe the specific assets and liabilities that are reported in financial statements.

In the Coinage Act of 1792 a unit of measure is in the form of weight of the silver, gold or platinum in a coin in the form of grains, grams.

To function as a ‘unit-of-account’, whatever is being used as money must be

|

Money acts as a standard measure and common denomination of trade. It is thus a basis for quoting and bargaining of prices. It is necessary for developing efficient accounting systems.

In the Financial Accounting Series in the Accounting Standards Update No.- 2011-04 of May 2011 entitled Fair Value Measurement (Topic 820) Amendments to Achieve Common Fair Value Measurement and Disclosure Requirements in U.S. GAAP and IFRSs and are form the Financial Accounting Foundation, 401 Merritt 7, Norwalk, Connecticut 06856 the term UNIT-OF-ACCOUNT states on page 15 of the document that « The unit-of-account represented by the transaction price is different from the unit of account for the asset or liability measured at fair value.«

Source: http://www.fasb.org/jsp

View Also Fair Value Measurement

Due Diligence On Guarantee 1 – 250M x 3

(3 times)

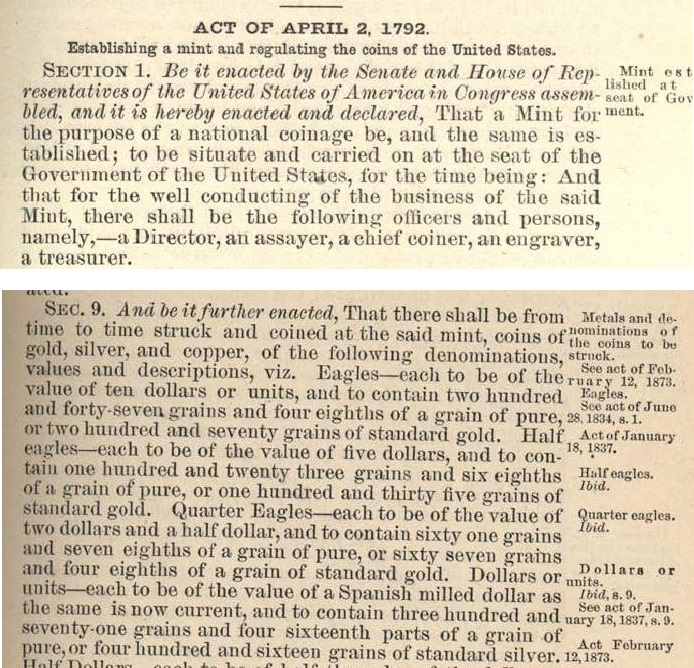

The “Coinage Act 1792” states “Dollars or units. Dollars or the same is now current, and to contain three hundred and seventy-one grains and four sixteenth parts of a grain of pure, or four hundred and sixteen grains of standard silver,…”

and from the original image text of 1792. The Section of the Coinage Act of 1792 with definition for “dollars or units” above in the picture is in yellow below.

Source http://www.usmint.gov/historianscorner/?action=docDetail&id=326

|

|

This yellow section is to highlight the section of the Coinage Act of 1792 above.

“Dollars or units – each to be of the value of a Spanish milled dollar as the same is now current, and to contain three hundred and seventy-one grains and four sixteenth parts of a grain of pure, or four hundred and sixteen grains of standard silver. »

EVIDENCE NUMBER 1

See Coinage Act of 1792 Section 9 and 20

Section 9. is with the evidencing of the these words “Dollars or units – each to be of the value of a Spanish milled dollar as the same is now current, and to contain three hundred and seventy-one grains and four sixteenth parts of a grain of pure, … standard silver…”

Section 20. “And be it further enacted, That the money of account of the United States shall be expressed in dollars or units, dismes or tenths, cents or hundredths, and miles or thousandths, a disme being a tenth part of a dollar, a cent the hundredth part of a dollar, a mille the thousandths part of a dollar, and that all accounts in public offices and…”

See website http://www.usmint.gov/historianscorner/?action=docDetail&id=326

See website again and view the original version download in Adobe PDF format since the MS Word format is not of the same wording.

http://www.usmint.gov/historianscorner/?action=docDetail&id=326

EVIDENCE NUMBER 2

|

Journals of the Continental Congress, 1774-1789 Page 499 and page 500 “Congress took into consideration the report of a grand committee, consisting of Mr. [David] Howell, Mr. [Abiel] Foster, Mr. [Rufus] King, Mr. [Joseph Platt] Cook, Mr. [Melancton] Smith, Mr. [John] Beatty, Mr. [Charles] Gardner, Mr. [John] Vining, Mr. [William] Hindman, Mr. [James] Monroe, Mr. [Hugh] Williamson, Mr. [Charles] Pinckney and Mr. [William] Houstoun, on the subject of a money unit. And on the question, That the money unit of the United States of America be one dollar, the yeas and nays being required by Mr. [David] Howell; Every member answering ay, it was Resolved, That the money unit of the United States of America be one dollar.” |

See website http://memory.loc.gov/cgi-bin/query/r?ammem/hlaw:@field(DOCID+@lit(jc0295))

“And text such as:

[Resolved] That the money unit of the United States, being by the resolve of Congress of the 6th July, 1785, a dollar, shall contain of fine silver, three hundred and seventy-five grains, and sixty-four hundredths of a grain.

From the broadside: « By the United States in Congress assembled. August 8, 1786 : On a report of the Board of Treasury… »

See website http://www.loc.gov/teachers/classroommaterials

EVIDENCE NUMBER 3

Testimony of James Ross Snowden was treasurer of the United States Mint from 1847 to 1850, and director of the Mint from 1853 to 1861

Question no. 76. “Upon what were the contracts in this country based up to that time? What unit of value was in use? – Answer; The dollar was the unit of value.”

Question no. 78. “Was not the majority of contracts based upon the Spanish milled dollar? – Answer; I have no doubt they were.”

Question no. 79. “How many grains of pure silver were in the Spanish silver dollar? – Answer; “Ah I think 371 and one quarter.”

Question no 80. “What was the unit standard of value previous to the passage of the mint law of 1792? – Answer; The Spanish-American Dollar.”

Question no. 81. “How many grains of silver were in that? – Answer; I think 371 and one quarter. I know the effort was made in the act of 1792 to hit exactly the Spanish-American Dollar.”

Question no. 82. “Then the question of Mr. Hamilton in framing the mint act of 1792 was not to create a new dollar, but to take as near as possible the value of the dollar actually in circulation and upon which contracts had been based? – Answer; Unquestionably so; the actual value.”

Question no 83. “…But as all contracts in this country prior to 1792 had been based upon the Spanish Milled Dollar…” continues

Question 83. “…value of silver in Spanish milled dollar debasement of the coinage and a fraud on the part of the founders of our republic to issue a dollar reduced to Spanish 371 and one quarter grains of pure silver?” Answer; “It was wrong in itself.”

See website https://books.google.ca/books

EVIDENCE NUMBER 4

|

By Ron Michener, University of Virginia

See website http://eh.net/encyclopedia/money-in-the-american-colonies/

Special note “EH.net is owned and operated by the Economic History Association with the support of other sponsoring organizations.”

http://eh.net/encyclopedia/money-in-the-american-colonies/

and the Economics History Association website is

http://eh.net/eha/about/2014-2015-eha-officers-and-board-of-trustees-2/

where-with The Officers and Trustees who overSee the Association are the following: President is Robert Margo, Boston University, President Elect is Lee Alston, Indiana University, Executive Director Price Fishback, University of Arizona, Immediate Past Presidents are Philip Hoffman, California Institute of Technology, Robert Allen, University of Oxford, Jeremy Atack, Vanderbilt University, Anne McCants, MIT Vice-President and Joseph Ferrie, Northwestern University, Stephen Broadberry, University of Warwick, Leah Platt Boustan, University of California, Los Angeles William Collins, Vanderbilt University

See page 103 as EXHIBIT D and many other pages of the book titled « International monetary conference », held in Paris, in August 1878, Reuben Eaton Fenton. Samuel Dana Horton. United States. Dept of State.

“…dollars or units each of the value of a Spanish milled dollar “like the dollar actually in circulation” and containing 371 and one quarter grains of pure silver…” and it continues to state “…in fact, and in the absence of a special law the Spanish dollars was probably from the beginning…” “…for all payments expressed in dollars…”

Page 103 and other pages

See website https://books.google.ca/books